The surge in digital wallet adoption is revolutionizing how payments are made. According to Juniper Research, digital wallets are expected to account for more than 50% of e-commerce transaction value globally by 2025.

Offering speed, security, and convenience, digital wallets have become indispensable for many consumers. At the same time, their ability to reduce cart abandonment, streamline payment flows, and enable international reach have created new revenue growth opportunities for merchants that leverage them.

To remain competitive, merchants must understand the factors fueling digital wallet growth, identify key players, and implement strategies to meet evolving consumer demands.

Why are digital wallets so popular with modern consumers?

Digital wallets allow consumers to store payment credentials from their credit or debit card digitally, allowing them to make payments without a physical card or cash. This simple feature of digital wallets provides the consumer with three key benefits:

- Convenience: Consumers can save all of their various payment methods — from credit and debit cards to bank accounts — in one place.

- Speed: Consumers can pay for things instantly with just a tap or click.

- Security: Advanced features like encryption, tokenization, and biometric authentication significantly reduce fraud risks and increase user confidence.

Who is using digital wallets and why?

While digital wallet usage is ubiquitous, certain consumer segments have been gravitating towards them:

- Millennials and gen Z - often regarded as digital natives, young consumers value the practicality and convenience of digital wallets. In fact, 79% of Gen Zers report using digital wallets regularly. They gravitate toward wallets that integrate with loyalty programs, social platforms, and budgeting apps, transforming routine transactions into engaging, multi-functional experiences.

- Freelancers and independent contractors - digital wallets have helped sustain the rapid growth of the gig economy by offering gig workers a way to instantly access funds, and track and manage their expenses.

- Unbanked and under-banked communities - In regions like Southeast Asia, Latin America, and parts of Africa, where traditional banking infrastructure is limited, digital wallets provide secure payments, savings, and access to the broader digital economy.

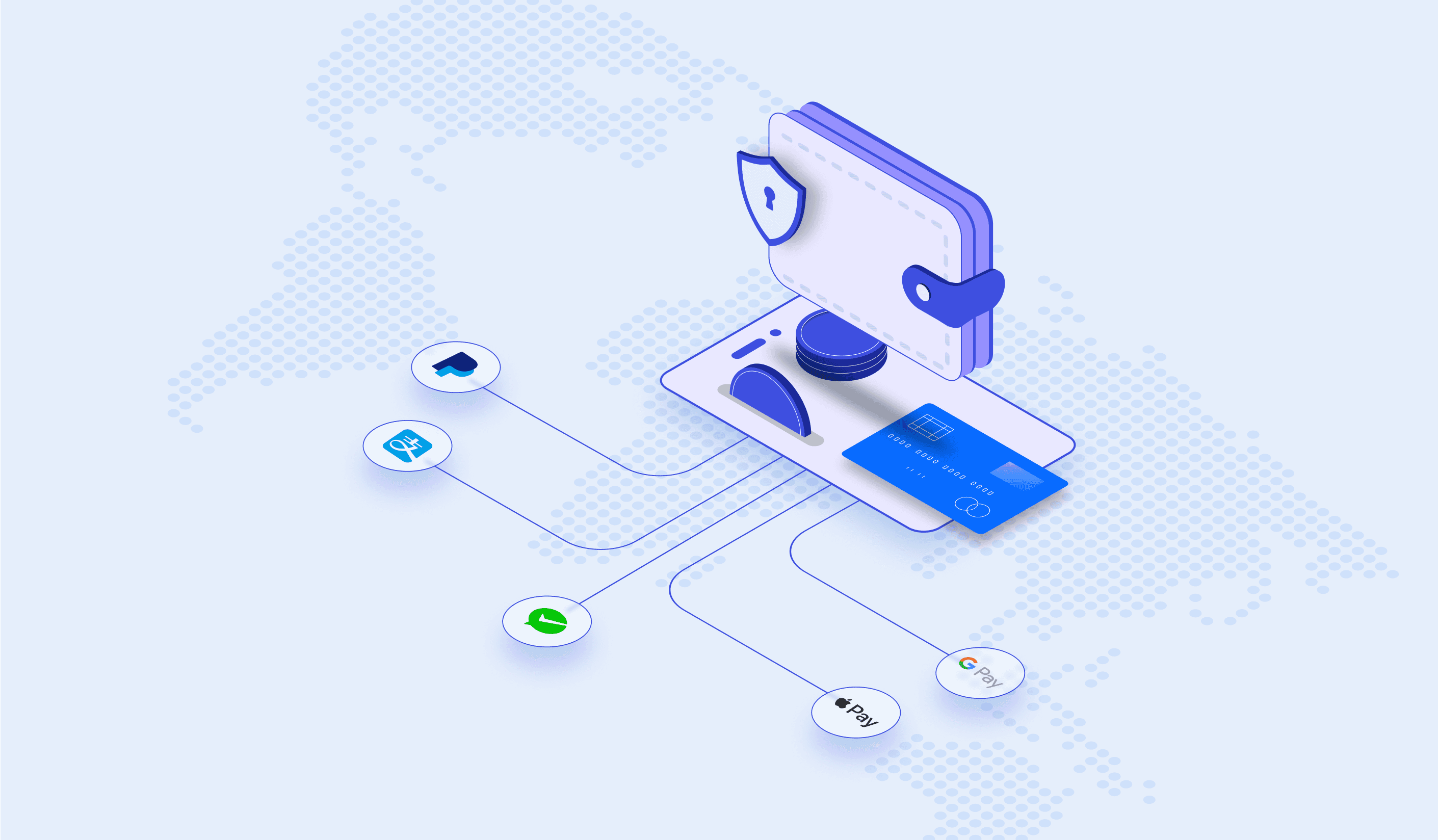

Key digital wallet providers to keep an eye on

The digital wallet market is dominated by global and regional leaders, each offering tailored solutions for specific user bases and payment needs.

- PayPal: A global pioneer in digital payments, supporting secure e-commerce and peer-to-peer transactions worldwide.

- Apple Pay: Known for its secure and user-friendly design, favored by iOS users for contactless and online payments.

- Google Pay: Catering to Android users with widespread compatibility and seamless integration within Google’s ecosystem.

- Alipay: With over 1 billion users, it dominates China’s commerce ecosystem and is expanding internationally.

- WeChat Pay: Embedded within the WeChat app, it offers seamless peer-to-peer, in-store, and online payments.

- Mercado Pago: A leader in Latin America, supporting e-commerce and in-store payments with solutions tailored to regional needs.

- Paytm: Driving India’s cashless revolution with UPI-driven payments, widely adopted for small merchants and bill payments.

- Klarna: A European leader offering wallet functionality combined with Buy Now, Pay Later (BNPL) options.

Integrating multiple digital wallet providers with Yuno

While it’s clear that digital wallets are a critical path for payments revenue growth, the big question is: which digital wallets should you integrate and how do you manage them?

Integrating multiple digital wallet providers can be a complex process, especially for businesses operating across diverse regions with varying consumer preferences. Each digital wallet has its own set of integration requirements, data privacy, and regulatory compliance standards, adding additional layers of complexity into a merchant’s payment stack.

This is why merchants use payment orchestration platforms like Yuno to streamline digital wallet integration, making the process efficient and hassle-free.

With Yuno, businesses gain access to a unified platform that connects hundreds of global and regional digital wallets through a single API. This approach eliminates the need for multiple integrations, reducing complexity and saving time. Merchants can onboard popular wallets like Alipay, Google Pay, and Mercado Pago, in record time.

By partnering with Yuno, merchants can focus on improving customer experiences while avoiding the technical complexities of integrating and managing digital wallets.

What’s next for digital wallets?

Digital wallets have already transformed how people transact; however, their evolution is far from over. Emerging technologies and shifting consumer expectations are driving exciting advancements in the digital wallet landscape. Key trends shaping the future include:

- Super Apps: Wallets are transforming into comprehensive ecosystems, combining shopping, transportation, and financial services within a single platform, offering unmatched convenience for users.

- AI-driven personalization: Artificial intelligence will enable tailored financial products, personalized rewards, and budgeting tools, enhancing the user experience and making financial management simpler.

- Biometric authentication: Fingerprint, facial recognition, and voice technology will enhance both security and ease of use, providing peace of mind for users.

These innovations promise to make digital wallets even more versatile, secure, and indispensable in the years ahead.

The rise of digital wallets represents a transformative shift in the payments landscape. By understanding the factors driving adoption, identifying key players, and leveraging integration solutions like Yuno, businesses can meet evolving consumer demands.

With Yuno’s seamless platform, merchants can easily adopt digital wallets, ensuring they remain competitive in a rapidly changing market.

Are you ready to embrace the digital wallet revolution with Yuno? Book a demo today.