The checkout is a critical piece of businesses’ revenue since it’s the moment all investments per customer will come true: all the time and aspects that caught the client’s attention perhaps won’t be enough for a successful buy. Frictions in the checkout flow, unnecessary transactions, and payment operation costs can contribute negatively to this situation. Without Payment Orchestration, there’s the need to use outdated solutions or maintain a payment engineering team to deliver and constantly iterate payment operation functions, which is a heavy and expensive engineering effort.

What is payment orchestration?

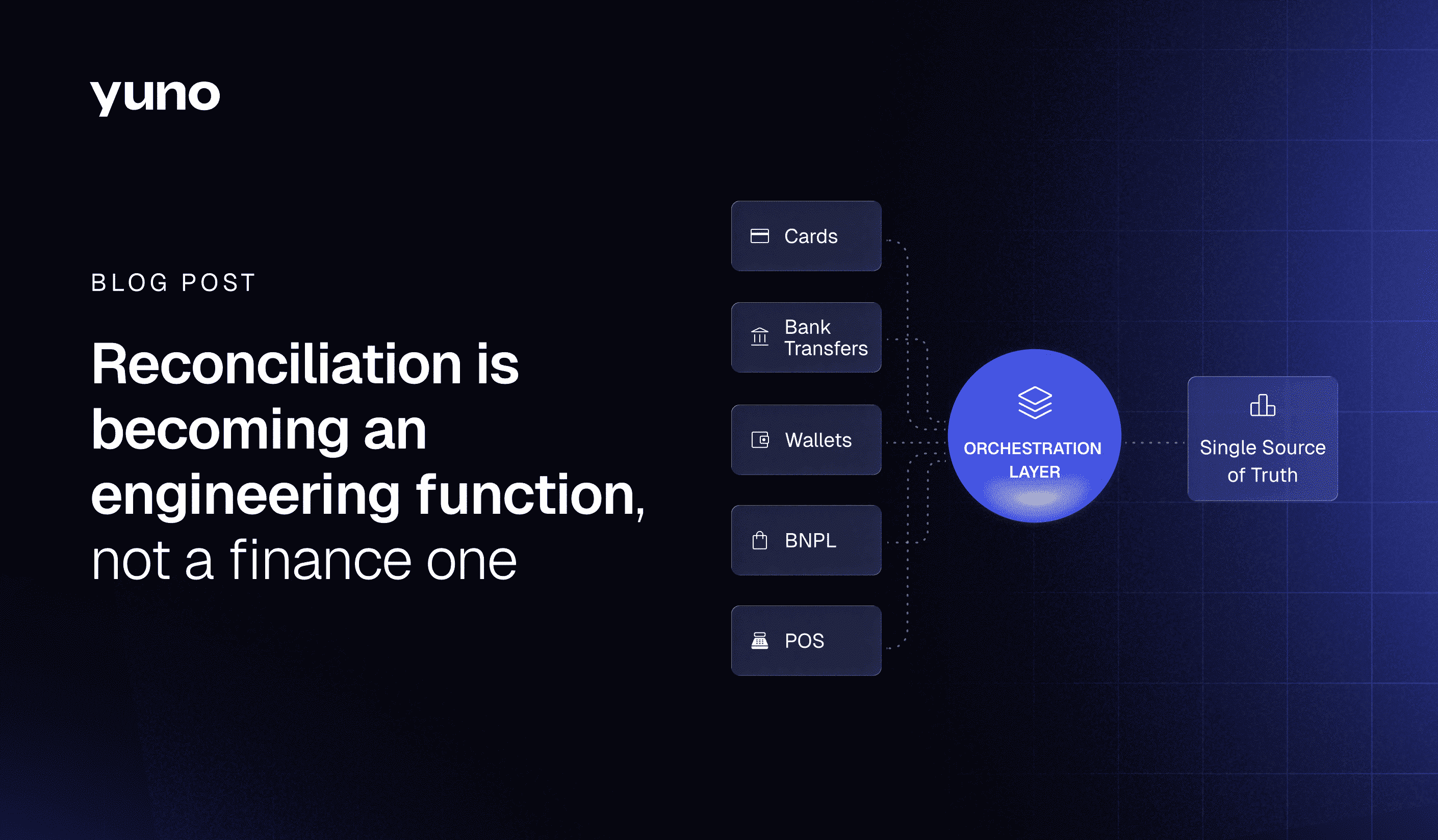

Payment Orchestration Platforms (POPs) have been created to simplify the complexity of payment processing into a unique, simple integration through outsourced software, reducing the IT team’s responsibilities. Merchants can elaborate rules for certain transactions, choosing the lowest fees or the highest possibility of approval: If an institution denies a transaction, POPs can try other payment processors multiple times. Using alternative payment processors makes buyers less frustrated since the process will be much faster and less likely to fail, contributing to less checkout abandonment.

Payment orchestration vs. payment processing

Payment service processors (PSPs) are companies that work with credit and debit card transactions, in which several steps and entities are needed in order to process a payment. Typically, merchants deal with numerous PSPs together in order to better fulfill their business’ payment processing needs. The main difference between these two is that POPs are an outsourced unified software that integrates different PSPs within, while PSPs required an integration of their own.

Compared to using PSPs alongside, when developing digital payment solutions, POPs give merchants more control and flexibility, raising their logistics scalability regarding payment rules. As shown by the 2020 MRC Global Payments Survey¹, there are several reasons for merchants to add new and local types of payment methods, and regarding them, POPs can:

- Help to reduce payment fraud by allowing customers to test fraud detection with diverse 3DS rules and fraud providers

- Improve customer experience and minimize checkout abandonment by optimizing checkouts

- Adopt more alternative payments, including mobile payment methods

- Expand the business to new markets by having access to dozens of payment methods through a single integration

- Meet regional payment requirements

- Reduce operational costs by outsourcing the payment orchestration

How Yuno’s POP goes beyond

Yuno’s Unified Solution offers several tools to ease merchants’ payment orchestration in a user-friendly environment making an easygoing flow a reality, among others:

- Global payment ecosystem;

- Accessibility and flexibility through interactive UI;

- Seamless one-click User Experience by visual programming;

- Tools to group and conciliate transactional data through the dashboard, consolidating analytics, sales, and declines;

- Smart Routing.

Check our article on Unified Payments for your Business with Yuno to get to know more about our approach and how we are revolutionizing payment orchestration in LATAM.